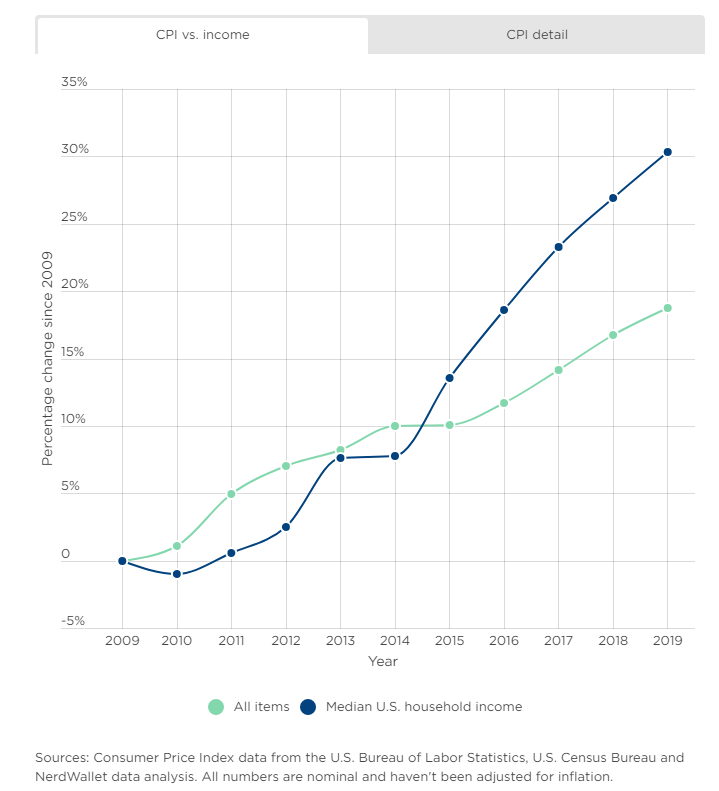

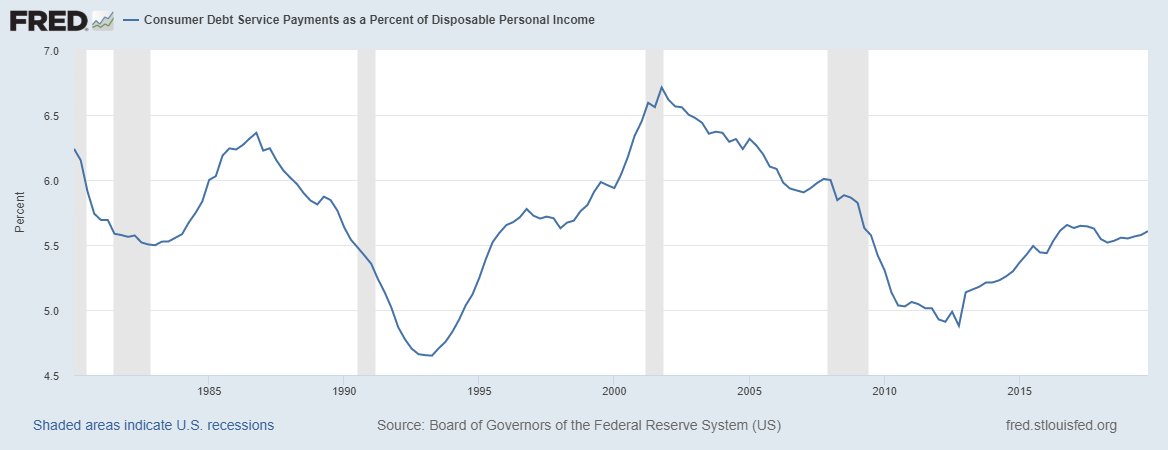

“It’s puzzling to me that if the economy is doing so well and that we’re so close to full employment, that consumer confidence is up … that we haven’t seen the numbers move much in people’s ability to save,” said Bruce McClary, spokesman for the National Foundation for Credit Counseling.