Did you know that when it comes to credit scores, usually higher earners have a higher score and lower earners have a lower score?

When it comes to credit scores and getting more credit, net-worth and how much you earn 100% effects this area of your life as well, in this article I want to focus on some of the credit score, rate and geographical differences we see between higher earners and lower earners.

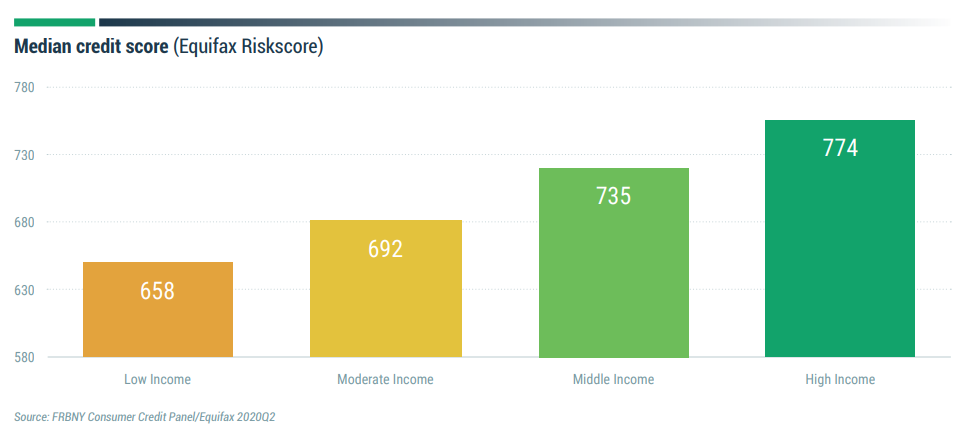

It is definitely like what you would assume with much of this data, the more money you make the higher your score usually is and the lower income earners tend to fit into the sub-prime category. The last few years have been extremely good to CEOs and company founders while punishing the middle and low earners. We saw top tech CEOs from Bezos to Musk pull out record high amounts of money through 2021, while we saw record high amounts of small businesses close.

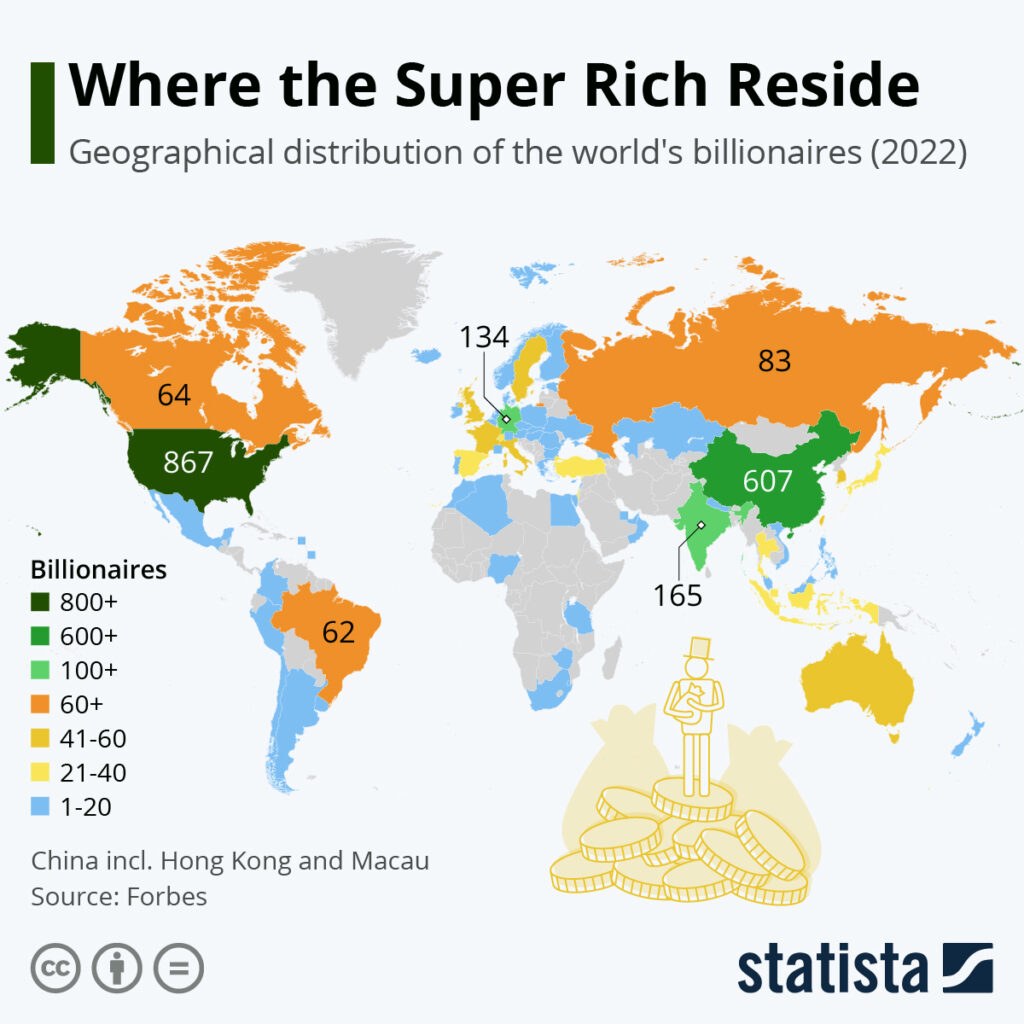

According to the Forbes Billionaires List of 2022, most of the world’s richest people are at home in the United States. As the Statista chart below shows, the country counted 867 billionaires per the list’s last release Tuesday. This is several more than the second-ranked country, China, with 607 and many more than in third-placed India with 165.

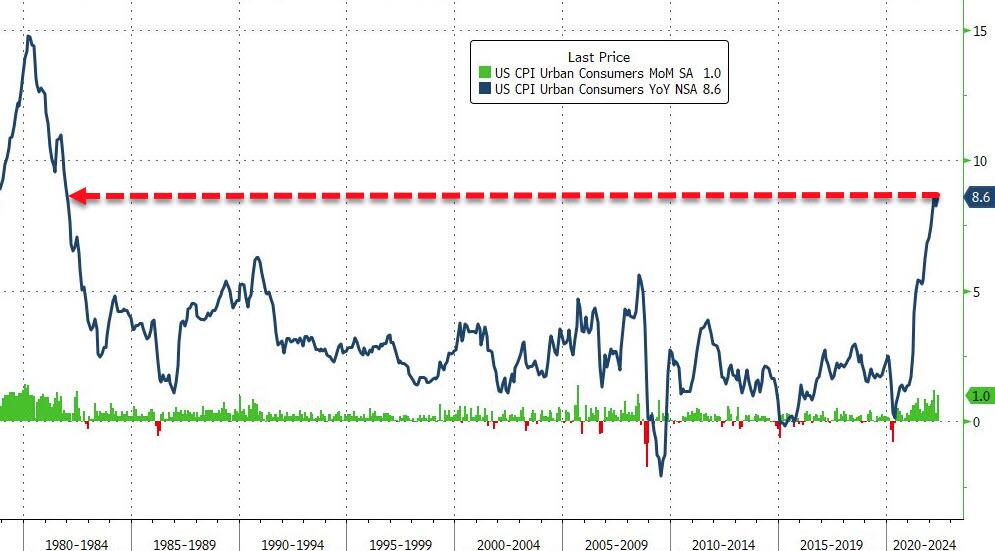

Inflation and money printing are two huge factors to inequality because it tends to push individuals up or down in terms of social structure. The last 2 years we have seen historic amounts of money printing and CPI we haven’t seen since 1981, the result of that is lower earners are pushed further down and higher earners are pushed higher up.

Lets star with some overall stats that are great to see…

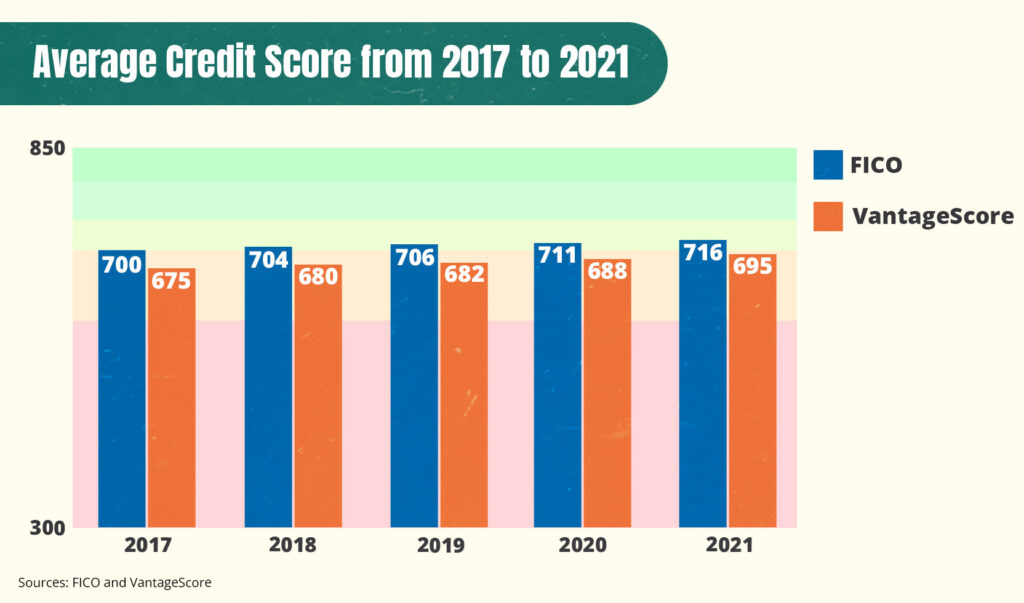

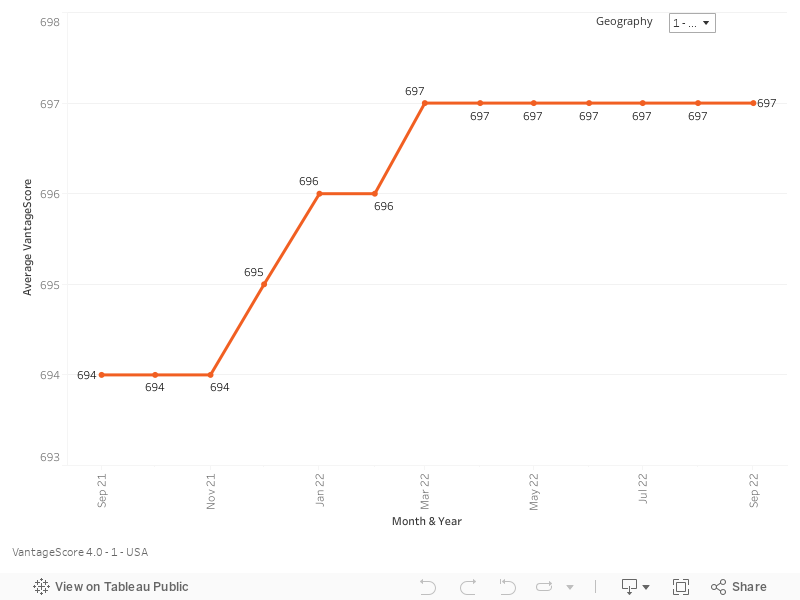

Currently, the average FICO score in the US is 716, and the average VantageScore credit score is 697, both of which are considered good credit scores.

The national average credit card utilization rate in 2021 is 25%, which is the lowest rate in at least a decade, that started in 2020.

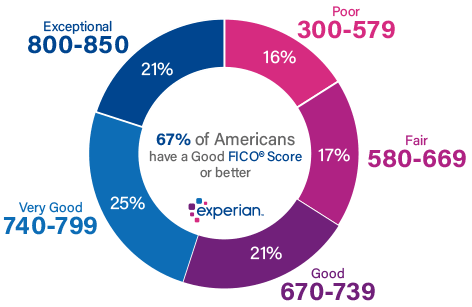

- 21% of Americans have over an 800 credit score

- 33% of Americans have a fair or poor credit score, putting them in subprime category

- 67% of Americans have a good, very good or exceptional score

They are also the largest share of perfect credit scores

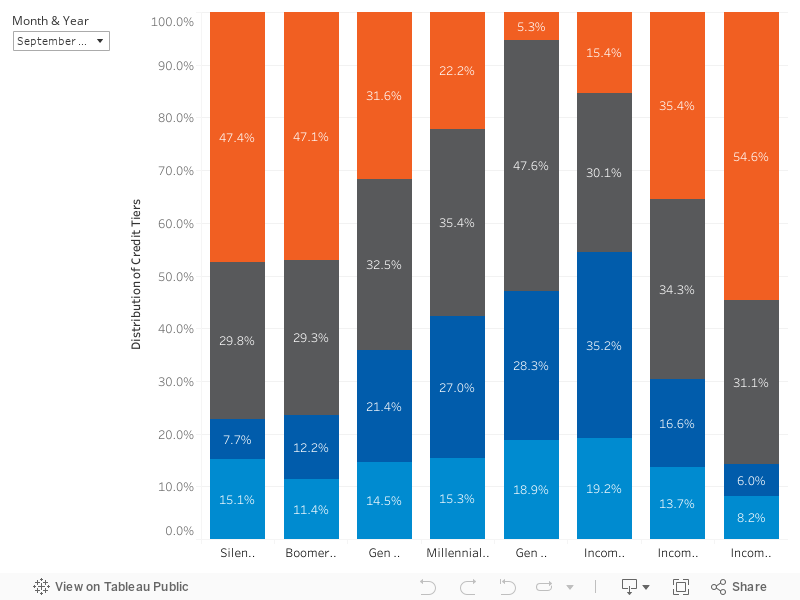

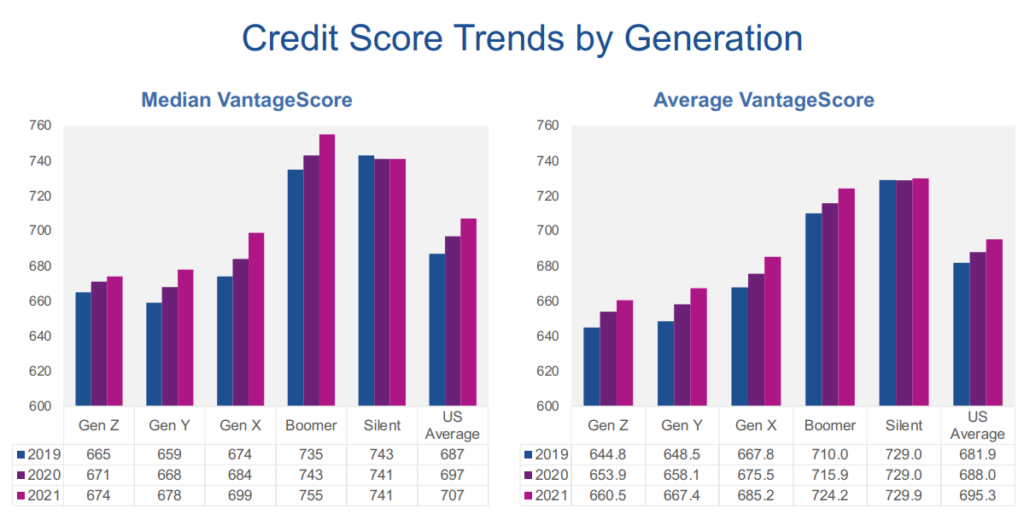

You can see in the chart below, the Boomer and Silent generation have the highest Vantage scores but this is also true for FICO. Baby boomers held the majority of perfect credit scores, accounting for 58% of people with an 850, according to Experian data from the fourth quarter of 2018. Generation X came next, accounting for 25% of people with perfect scores, and the silent generation trailed with 13% of the best scores.

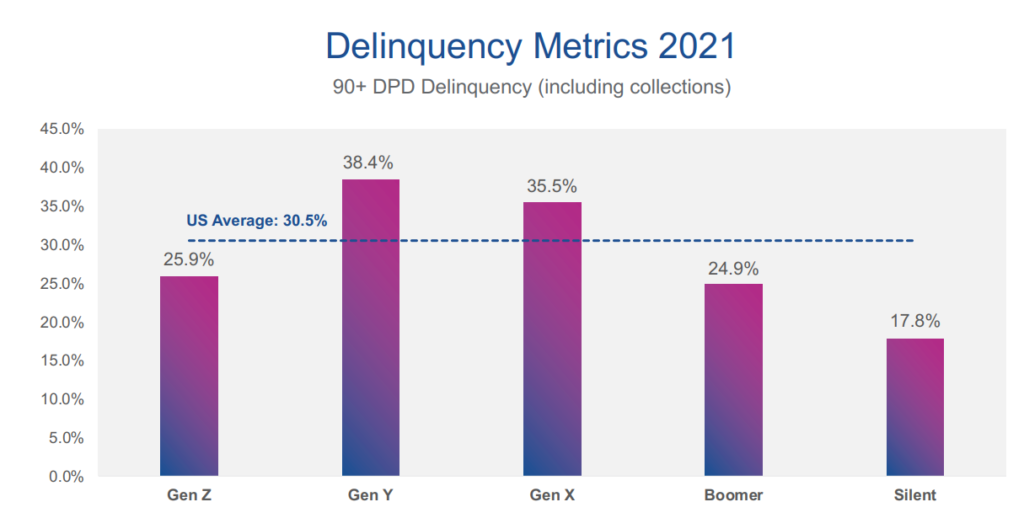

Older generations also carry the most amount of credit cards (boomers 3.4 average), Silent generation averages $3,821 credit card balances vs $7,236 for Gen X and have the lowest amount of delinquency/defaults according to 2021 Experian data.

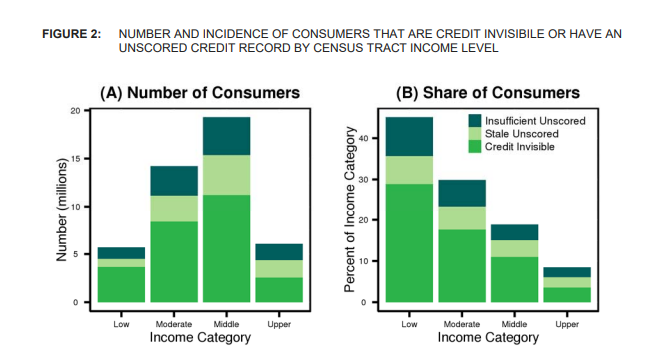

Nearly 50% of low-income adults are credit invisible or not scorable.

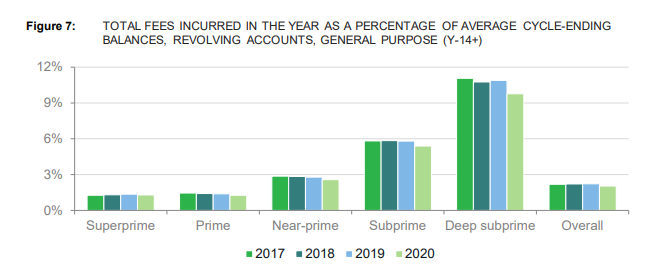

And low credit score individuals tend to pay more in fees…

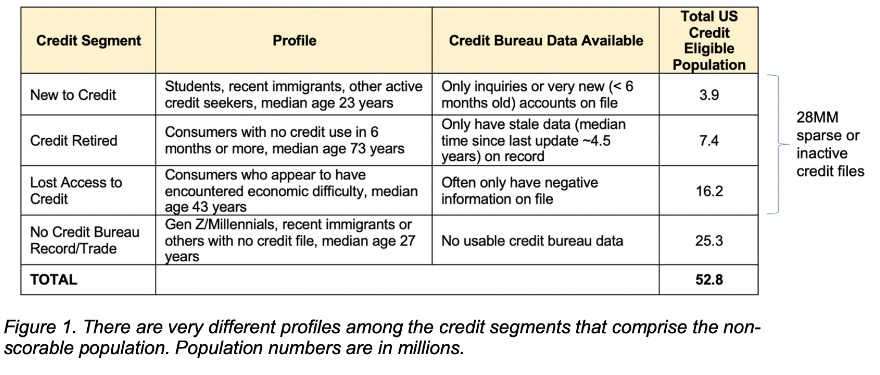

So there is a total of 258M people according to Census data that are eligible for credit, out of that 232M people can be scored by FICO, which leaves out roughly 53M people who have only scant credit bureau data or no data at all. Finally out of that 53M people, 25M of them are what’s called ‘credit invisible’, with no credit bureau record at all.

This means either no credit score, no credit history or inactive credit files.

According to VantageScore, 37M more consumers are scorable with Vantage3.0 and 4.0 scoring models, that were previously invisible using ‘legacy models’. 13M of these consumers have VantageScore credit scores of 620 or higher;

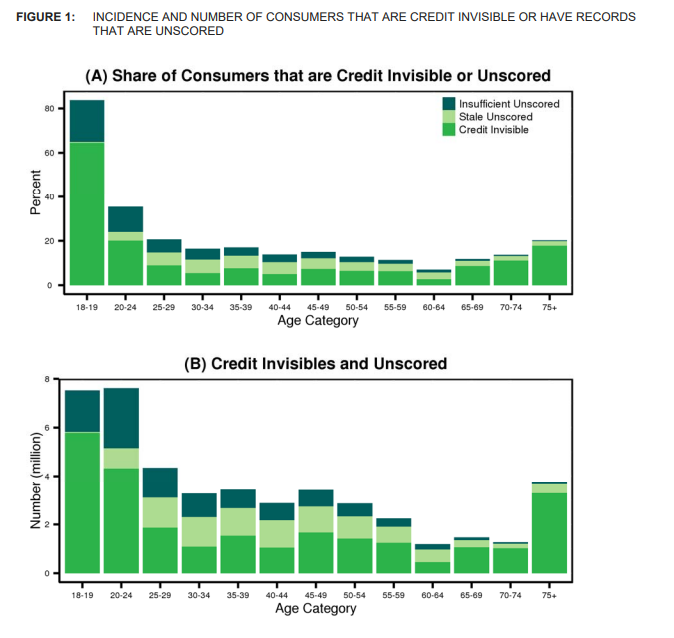

The Consumer Financial Protection Bureau (CFPB) found that in 2010, 26 million adults in the US were “credit invisible” (meaning they had no credit files or records of credit activity at all), accounting for approximately 11% of the adult population.

In 2010, 19M adults were “unscorable” due to an insufficient credit history (too few credit accounts or not enough recent account activity) according to the CFPB.

As shown, over 80% of 18 or 19 year old’s are credit invisible or have unscored records. This

percentage drops substantially for older consumers, falling below 40% in total for the 20

to 24 year old age group. After age 60, the number of consumers that are credit invisible or that

have an unscored record increases with age.

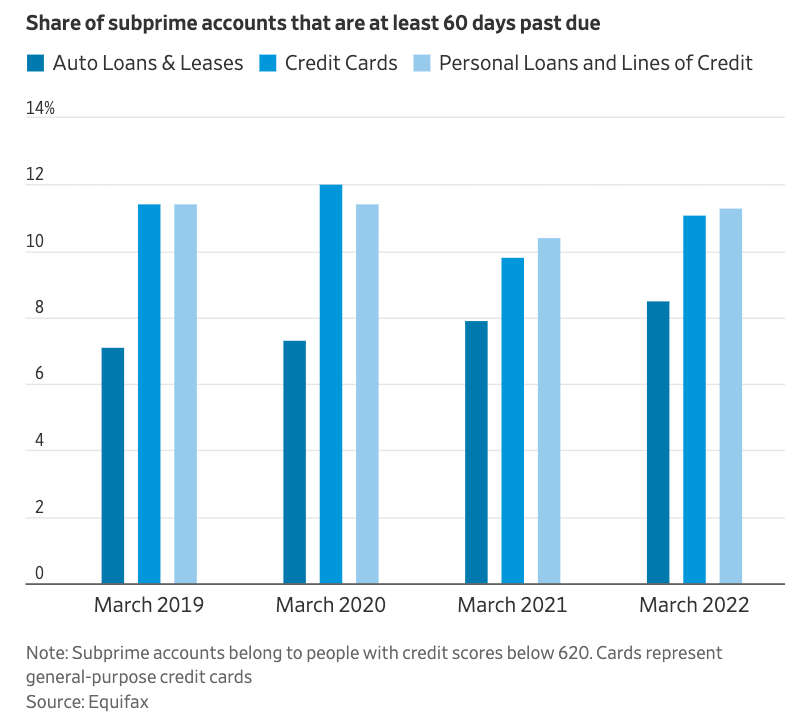

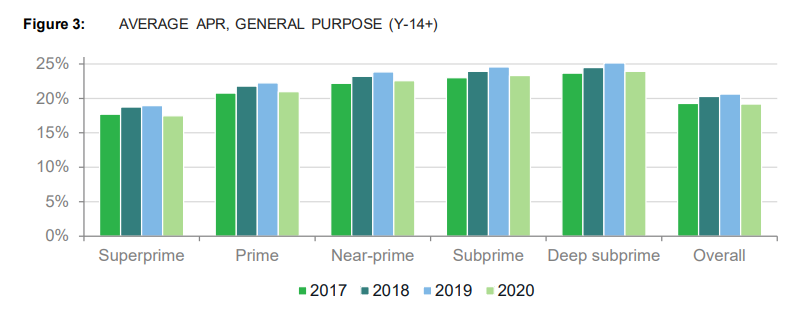

This is the most recent sub-prime delinquency data I could find which is up to March 2022.